You've spent years building your retirement accounts, carefully balancing today's life with tomorrow's dreams. Maybe you're thinking about retiring in five years, or maybe you're ready to take the leap. Either way, you know the drill: stocks are for growth, cash is for short‑term needs, and somewhere in the middle... bonds?

Bonds often feel like the awkward middle child of your portfolio—too boring to excite you, but too important to ignore. Here's the reality: when markets turn ugly, it's often the mid‑term bucket that determines whether you can stay calm, stick with your plan, and avoid selling stocks at exactly the wrong time.

Picture your money in three buckets:

In a bull market, you refill your short‑term bucket from the long‑term bucket. You sell some winners, take the gains, and life is good.

In a bear market, the mid‑term bucket steps in. Instead of panic‑selling stocks when they're down, you pull from your bond bucket, giving your long‑term investments time to recover. That's the quiet superpower: it lets you spend what you need without wrecking your long‑term plan.

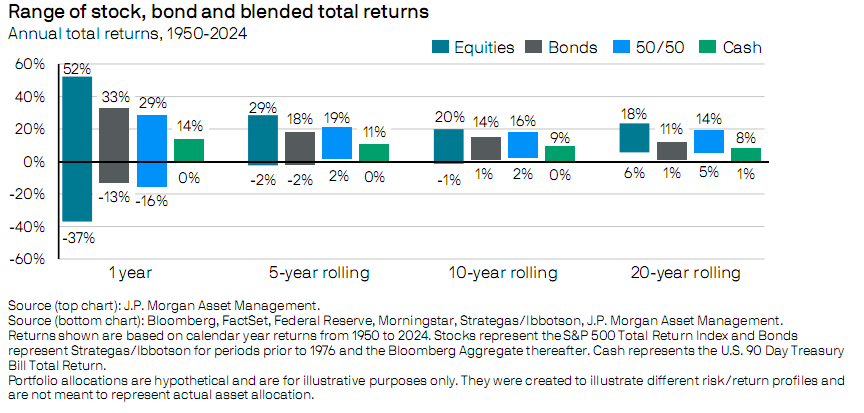

The classic "range of returns" chart tells the story. Over any given year since 1950, U.S. stocks have swung from roughly –37% to +52%, while bonds have lived in a much narrower band; a 50/50 stock‑bond mix sits in between and looks smoother.

Your mid‑term bucket isn't there to beat stocks—it's there to:

Bonds aren't magic. They can still lose value, especially when interest rates spike (hello, 2022). But over time, a mix of bonds and stocks can be far calmer than stocks alone.

Duration measures how sensitive your bonds are to interest rate changes. If a bond fund has a duration of 6 years, a 1% jump in rates might mean about a 6% price drop. Most mid‑term buckets use intermediate‑duration bonds (4–7 years)—not cash, but not nearly as wild as stocks.

Many bond funds track the Bloomberg U.S. Aggregate Bond Index ("the Agg"), which is quoted on a 100‑point scale. Below 100 means bonds are trading at a discount; above 100 means a premium. When funds like AGG trade under 100, you're buying at a discount, and over time you get both interest payments and a "pull‑to‑par" gain as bonds mature.

After recent rate spikes, bond prices fell and yields rose. Uncomfortable? Yes. But it also means starting yields and expected returns are now higher than when yields were near zero.

Municipal bonds (munis) are the celebrities of the bond world: “tax‑free income!” sounds glamorous. But whether that actually helps you depends heavily on your tax bracket and account type.

A quick rule of thumb is the tax‑equivalent yield:

Tax‑equivalent yield ≈ muni yield ÷ (1 – your marginal tax rate).

If a muni fund yields 3% and you’re in a 24% bracket, the tax‑equivalent yield is:

3%÷(1−0.24)=3%÷0.76≈3.95%

So a taxable bond fund would need to yield around 3.95% to match the muni fund after taxes.

Munis can be very useful when:

For many households in moderate brackets, or for money held in retirement accounts, a straightforward taxable bond fund can be just as effective—or better—after tax, once you factor in fees and risk. That doesn’t make munis “bad”; they’re just a niche tool, not a universal default.

Here's a snapshot using recent data. This is education only, not recommendations.

*Based on data from Yahoo Finance as of 5/5/2026. Yields and volatility are approximate and change over time; always check current data before doing detailed analysis.

If you like visuals, you can view a side‑by‑side total return chart for AGG, BND, BNDX, and PIMIX (with dividends reinvested) from 2013–2026 at totalrealreturns.com.

When markets are calm, the mid‑term bucket feels invisible. When things get ugly, it's what lets you:

Bonds won't make you rich. They can still have rough years. But when you and your partner are sitting at the kitchen table during the next bear market, it's usually not the flashy part of your portfolio that saves you—it's the quiet middle bucket that keeps everything from falling apart.

Want to talk through how your three buckets should look for your specific situation? Whether you're a few years out from retirement or already living it, let's build a plan that works for both of you. Book a no‑pressure chat here: https://calendly.com/prudence-zhu/30min