When Life Changes, Your Plan Should Too: How to Turn Good Intentions into Action ✨

Prudence Zhu

CFP®, CPA, CFT™

Posted on:

December 17, 2025

Money isn’t just about numbers on a spreadsheet. It’s about choices, freedom, security, and the ability to live a life that actually feels like yours. As a fee‑only holistic financial planner at Enso Financial, the work centers on helping you make confident choices with your money AND feel good about them.

Why financial planning actually matters 🧭

Financial planning is how you connect your money to your real life: your values, goals, and responsibilities. Instead of wondering in the dark, “I hope I'm doing this right,” you get a clear roadmap that answers questions like:

Can I afford to change careers, start a business, or reduce my hours?

Are we on track for retirement and the things we want to do before then?

How do we balance paying off debt, saving, investing, and actually enjoying life now?

Good planning goes way beyond charts and projections. It helps you understand trade‑offs, make decisions on purpose instead of in panic mode, and adjust when life inevitably changes. A strong plan turns vague money worries into specific next steps, and that is where peace of mind really begins.

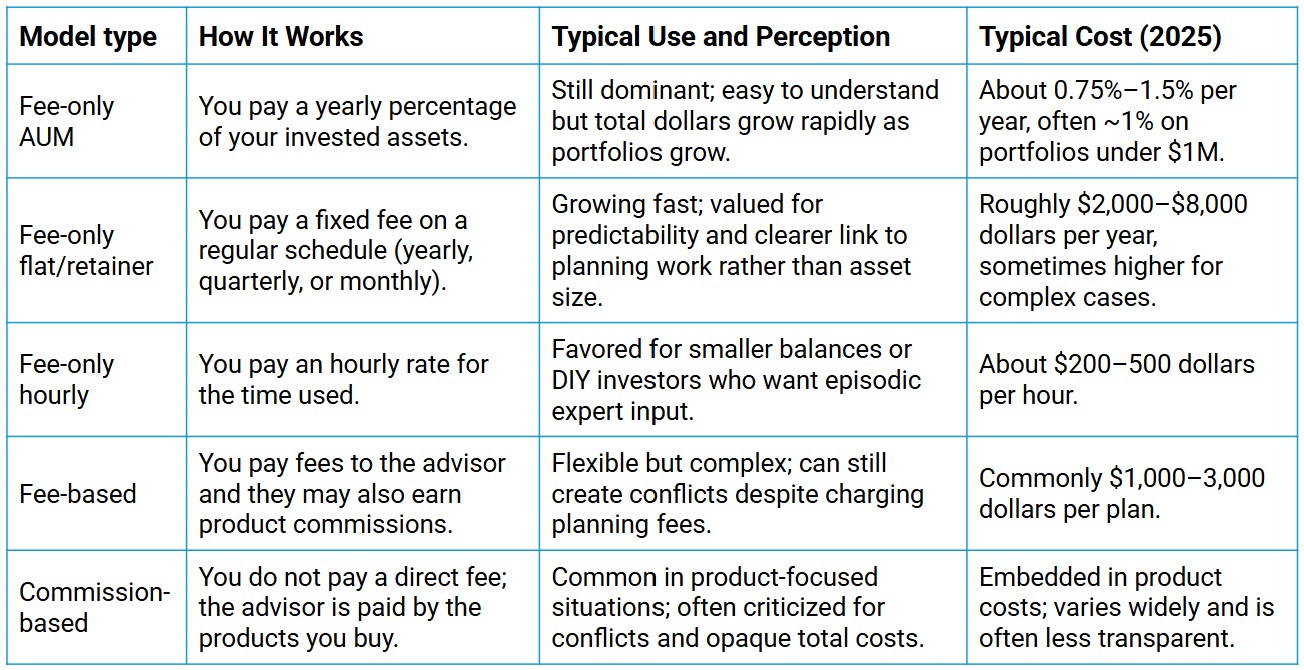

What fee-only really means (and why it matters) 💡

“Fee-only” simply means the planner is paid only by clients, never by product providers like mutual fund companies, or annuity or insurance carriers. There are no commissions, no sales quotas, and no “If you buy this, I get paid extra” hiding in the background.

That’s different from:

Commission or product-based: The advisor gets paid by selling certain investments or insurance products. This can create pressure (even unintentionally) to recommend items that pay more, not necessarily what’s best for you.

Fee-based: This sounds similar to fee‑only, but it is not the same. Fee‑based advisors can charge fees and also receive commissions. You may pay a planning fee and still have product compensation lurking in the background.

Fee‑only does not make a planner perfect, but it does simplify the relationship. You are paying for advice, not a sales pitch dressed up as advice. That clarity is a huge part of financial empowerment. Because you deserve to know exactly who your planner works for.

To put all of this in context, here’s how the main advisory pricing models generally work today and what they typically cost:

How Financial Advisers Get Paid Today

Why more advisors are charging for planning now 📈

For years, many advisors treated financial planning as a “freebie” attached to investment management or product sales. In 2020, roughly 28% of advisors still gave planning away. By 2023, that dropped to about 10%. That’s a big change, and it’s not an accident.

Several things are driving this shift:

Clients want real planning, not just investment picks. People need help with student loans, equity compensation, career moves, family support, and life transitions. That work requires time, skill, and ongoing attention.

Technology made “just investing” cheaper. If an advisor only picks funds, it is hard to justify a large fee. The real value today lies in planning, guidance, and support for behavior change, not simply in placing trades.

Advisors are recognizing the depth of the work. True planning involves detailed data gathering, scenario modeling, tax awareness, accountability, and follow‑through. Giving all of that away for free is not sustainable and it signals that planning doesn’t matter, which is the opposite of the truth.

Transparent planning fees are actually a win for clients. You can see what you are paying for, and planners are encouraged to invest more energy in what helps you most: thoughtful, personalized, ongoing advice.

How Enso Financial serves clients 🌱

At Enso Financial, the focus is on holistic financial planning, which means starting with you, not with products or portfolios. The goal is to empower you to envision and live a life that feels aligned, and then build a financial structure to support it.

In practice, that looks like:

Life planning that puts your “why” before your “how.” Together we clarify what you truly want your money to do for you, including your values, goals, priorities, trade‑offs, and the big‑picture direction of your life and work.

Comprehensive financial planning that builds the framework to support that life. This includes cash flow, debt management, saving strategy, tax awareness, investments, insurance review, education and retirement planning, estate coordination, and major purchase or investment decisions.

Financial therapy–informed support that helps you actually live the plan. You have a structured space to explore your beliefs, emotions, and patterns around money so your strategy fits not only the spreadsheet but also how you truly think, feel, and behave.

A quarterly-in-advance retainer that keeps the relationship active and responsive. Instead of a one‑time plan that gathers dust, you receive ongoing guidance. Fees are billed quarterly in advance, with a typical annual range of $3,500 to $7,500 based on complexity, so you have a consistent partner rather than a one‑and‑done transaction.

What this means for you 🌈

Putting it all together, the value of working with a fee-only holistic financial planner at Enso Financial is simple:

The advice is focused on you, not products.

The relationship is ongoing, so you’re not left alone after getting a thick report.

The work covers both the technical side of money and the human side of behavior and meaning.

If you’re ready to move from “I hope this works out” to “I know why I’m making these choices and I like where I am headed,” that’s where this kind of planning shines.