This article launches our series of hypothetical client case studies, starting with one of the most common questions: When Can We Retire?

Couples in their late 50s in the U.S. can often retire when their projected income from investments, Social Security, and pensions—after accounting for taxes and healthcare—is sufficient to support their desired lifestyle for 35 years or more. This requires a thoughtful comprehensive plan, including investment and tax strategy, withdrawal strategy, and attention to Required Minimum Distributions (RMDs).

Hypothetical Couple Profile

Alex (59) and Kim (57) want to know if they can both retire around age 62. Together, they have $1.4 million in pre-tax retirement accounts, $200,000 in Roth IRAs, $150,000 in taxable savings, no high-interest debt, and plan to claim Social Security between ages 62 and 70. Their goals: $90,000 per year of after-tax spending, a paid-off mortgage by 62, detailed planning for healthcare costs, and aiming for a joint life expectancy into their 90s.

Key Questions

Is retiring at 62 financially sustainable, or would working longer help?

How should they coordinate Social Security, RMDs, and withdrawals from different accounts?

Should they consider Roth conversions, and how do those work?

How can investments fund near-term cash needs and support long-term growth while managing market risks?

Planning Framework

This case study centers on objective analysis: we address the couple’s goals, outline planning steps, and clarify desired outcomes through careful financial modeling and strategy. In future case studies, we’ll also highlight how we help clients with communication, provide emotional support, and offer behavior coaching to guide important financial decisions and transitions.

Cash-flow and asset review: Calculate retirement spending for housing, healthcare (including Medicare), taxes, travel, gifts, and donations. List all income sources—Social Security, pensions, part-time work—and all assets.

RMD rules: Most pre-tax retirement accounts (IRAs, 401(k)s) require RMDs starting at age 73 or 75, depending on birth year. In their case, both are born after 1960, so age 75 applies. RMDs are taxable and must be taken every year once they start; missing one can result in stiff IRS penalties up to 25%.

Social Security timing: Evaluate options such as claiming at full retirement age, claiming earlier, or delaying. Delaying the higher earner’s benefit can increase total and survivor income; but the optimal strategy has to take into consideration health, cash‑flow needs, and work plans.

Tax and RMD mitigation: Consider Roth conversions and strategic withdrawals before RMDs begin to lower future RMDs and taxes. Explore qualified charitable distributions (QCDs), which allow IRA holders over 70½ to meet RMDs with direct charity gifts.

Other tax strategies: Use asset location (placing investments to maximize tax efficiency), withdrawal sequencing (which account to draw from first), gifting strategies for family, donor-advised funds for immediate deductions, and monitor IRMAA (Medicare premium surcharges) with careful income management. More advanced strategies include charitable trusts, loss harvesting, and multi-year tax planning; collaboration with CPAs as wealth grows.

Scenario analysis: Model long-term outcomes, adjusting for inflation, market returns, retirement age, and spending. Test what happens in higher inflation or poor market conditions and identify ways to improve the odds through saving more, working longer, or spending less or later. These scenarios help determine whether the desired $90,000 after tax appears sustainable and what changes could improve the odds.

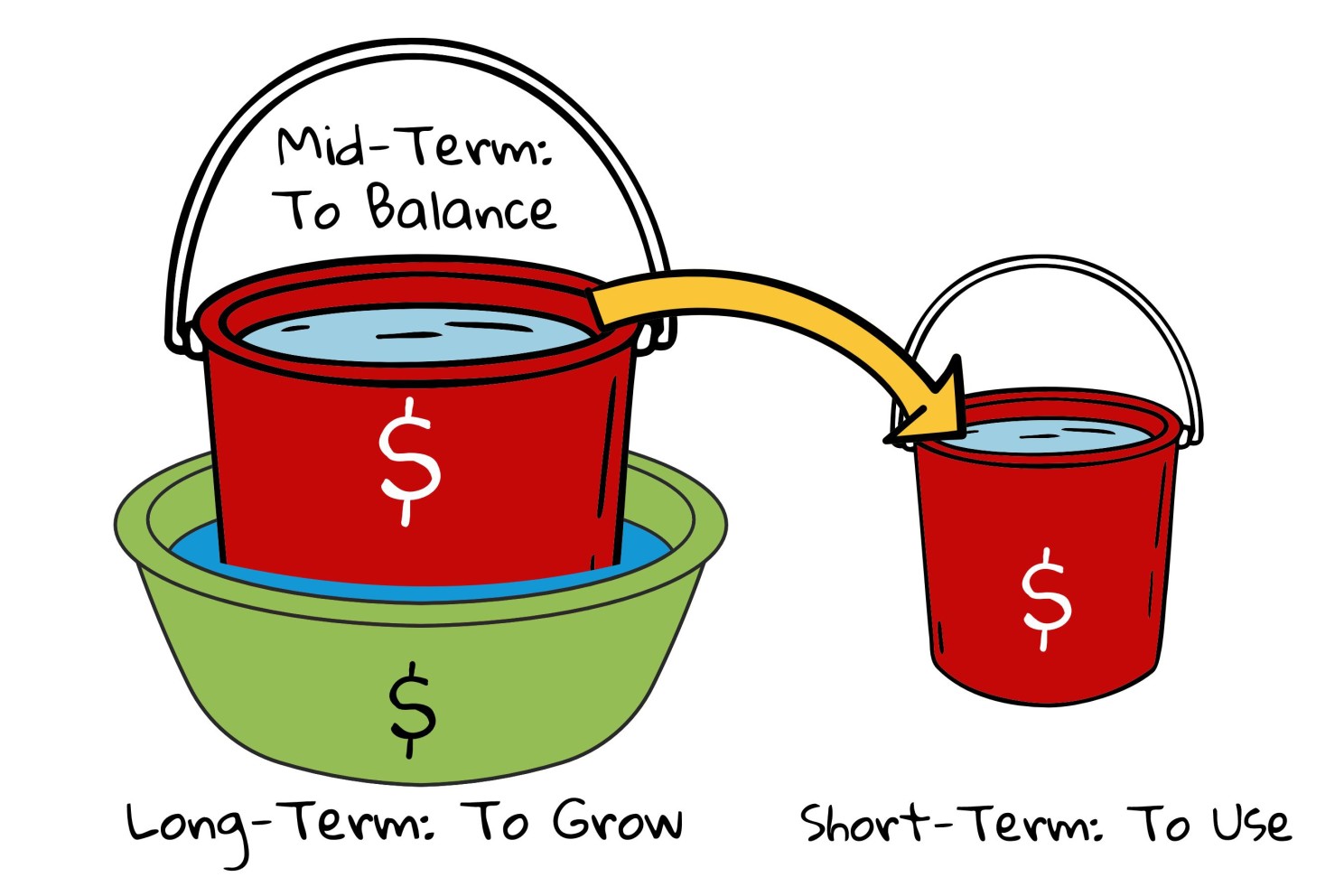

Three-Bucket Investment Strategy

To handle withdrawals and reduce market risk, Alex and Kim use a three-bucket approach:

Short-term (0–2 years): Two years of living expenses and taxes in low-risk, liquid accounts such as money markets or treasury bills.

Mid-term (3–7 years): Three to seven years of cash needs in a balanced mix of bonds and stocks for moderate growth with less volatility.

Long-term (8+ years): The rest in stocks and growth assets for long-term appreciation.

As RMDs begin, the plan moves those distributions into the short- or mid-term buckets, ensuring cash is available when needed and reinvests extras thoughtfully. Any RMD not immediately needed for spending can be reinvested in taxable accounts in the appropriate bucket, while taxes on the RMD are modeled in the cash‑flow plan.

Money Buckets: Use, Balance, Grow!

Desired Outcomes

Using this framework for the hypothetical couple, the planning objective is to:

Determine whether retiring at 62 with a $90,000 after‑tax spending target is projected to be sustainable under reasonable return, inflation, and longevity assumptions and, if not, quantify the effects of working longer, adjusting spending, or increasing pre‑retirement savings.

Coordinate Social Security timing, tax planning, and RMD management—potentially including pre‑RMD withdrawals or conversions—to help limit “RMD shock” and support more stable after‑tax income over time.

Maintain at least two years of withdrawals in conservative holdings, three to seven years in a balanced bucket, and the rest in growth assets, with a disciplined process for refilling buckets and meeting RMDs and other obligations without relying on market timing.

If you'd like to review your unique financial situation and explore your retirement options, book a complimentary 30-minute consultation here: http://calendly.com/prudence-zhu/30min. Take the next step toward clarity and confidence in your financial future.

Disclosure: This case study is hypothetical and does not represent any specific client. It is for illustration only to show the types of planning strategies a fee-only advisory firm may provide. Results vary; past performance does not guarantee future outcomes.